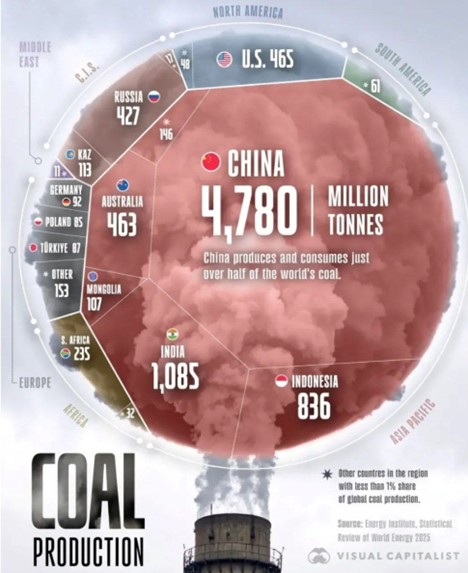

The global coal market remains highly concentrated, with the majority of production located in Asia. According to data from the Energy Institute (Statistical Review of World Energy 2025), China accounts for 4,780 million tonnes of coal per year—more than half of global production. This makes China not only the largest producer but also the leading consumer of coal. It extracts 4.5 times more than India and nearly 10 times more than the United States. This scale is driven by China’s energy structure, which still heavily relies on coal, despite massive investments in renewables.

India ranks second with 1,085 million tonnes, driven by growing industrial and residential demand for electricity. Indonesia, with 836 million tonnes, is largely export-oriented, supplying coal to Southeast Asia, China, and South Asia.

Among Western nations, the United States (465 Mt) and Australia (463 Mt) remain major producers. Despite green transition policies, both continue to maintain stable output— the U.S. primarily for domestic use, and Australia for export. Russia follows with 427 Mt, maintaining its status as a key player despite sanctions and reduced exports to Europe. Regional suppliers such as Kazakhstan (113 Mt) and Mongolia (107 Mt) continue to strengthen their positions, especially in supplying China.

In Europe, countries like Germany (92 Mt), Poland (85 Mt), and Turkey (87 Mt) continue coal production despite decarbonization goals, largely driven by energy security concerns and the need to replace natural gas imports after the 2022–2023 energy crisis.

In summary, Asia is the undisputed center of global coal production, accounting for over 75% of output. Asian countries are now key players in the global climate agenda, and any shift in their energy policies will have a direct impact on global emissions. The future of coal largely depends on decisions made in Beijing, New Delhi, and Jakarta.

* The Institute for Advanced International Studies (IAIS) does not take institutional positions on any issues; the views represented herein are those of the author(s) and do not necessarily reflect the views of the IAIS.